Time-itTime-it = Time based indicator

The Time-it indicator parses data by the day of week. Every tradeable instrument has its own personality. Some are more volatile on Mondays, and some are more bullish / bearish on Fridays or any day in between. The key metrics Time-it parses is range, open, high, low, close and +volume-.

The Time-it parsed data is printed in a table format. The table, position, size & color and text color & size can be changed to your preference. Each column parsed data is the last 10 which is numbered 0-9 which refers to the number of the selected day bars ago. For example: if Monday is chosen, 0 is the last closed Monday bar and 9 is the last closed Monday 9 Monday bars ago.

Range = measures the range between high and low for the day.

Open = is the opening price for the day.

High = is the high price for the day.

Low = is the low price for the day.

Close = is the closing price for the day.

+volume- = is the positive or negative volume for the day.

Default settings:

*Represents a how to use tooltip*

Source = ohlc4

* The source used for MA

MA length = 20

* The moving average used

Day bar color on / off

* checked on / unchecked off

Monday = blue

Tuesday = yellow

Wednesday = purple

Thursday = orange

Friday = white

Saturday = red

Sunday = green

Day M, T, W, TH, F, ST, SN.

* Parsed data for the day of week tables

Table, position, size & color:

Top, middle, bottom, left, center, right

* Table position on the chart.

Frame width & border width = 1

Text color and text size

Border color and frame color

Decimal place = 0

* example: use 0 for a round number, use 4 for Forex

*** The Time-it indicator uses parts and/or pieces of code from "Tradingview Up/Down Volume" and "Tradingview Financials on Chart".

ค้นหาในสคริปต์สำหรับ " TABLE"

Forex & Stock Daily WatchList And Screener [M]Hi, this is a watchlist and screener indicator for Forex and Stocks.

This indicator is designed for traders who trade in the forex markets and monitor developments in indices and other currency pairs.

It includes information on 14 indices such as the volatility index, Baltic dry index, etc. You can customize the indices as you wish. The indices table contains the index's price (or points), daily change, stochastic value, and trend direction.

The second table is designed for trading forex and stock currency pairs.

In this table, you will find information such as price, volume, change, stochastic, RSI, trend direction, and MACD result for all traded pairs. You can customize all the currency pairs in this table as you wish, and you can also tailor the oscillator settings to your preferences.

In the settings section, you can use checkboxes to hide the pairs in both tables.

The "Customize" section in the settings allows you to personalize the table appearances according to your preferences.

HTF Oscillators RSI/ROC/MFI/CCI/AO - Dynamic SmoothingThe Interplay of Time Frames: A Balanced View

Navigating the markets often involves interpreting trends from multiple angles. The HTF Oscillators with Dynamic Smoothing indicator enables you to do just that. This tool provides the option to integrate smoothed oscillator readings from Higher Time Frames (HTF) into lower time frame charts, such as a 1-minute chart. By doing so, the indicator offers a balanced viewpoint that bridges the gap between micro and macro perspectives, helping you make informed decisions without losing sight of the broader market context.

Features

Multi-Oscillator Support

Choose from a range of popular oscillators like the Relative Strength Index (RSI), Rate of Change (ROC), Money Flow Index (MFI), Commodity Channel Index (CCI), and Awesome Oscillator (AO). These oscillators are commonly used as foundational building blocks in trading strategy scripts by traders worldwide. Switch effortlessly between them, depending on your trading strategy and requirements. To maintain consistency and a familiar user experience, our script adopts the same visual aesthetics that you'll find in Pine Script indicators on TradingView: a sleek purple line for the oscillator and a transparent band filling. These visual elements are not only pleasing to the eye but also widely appreciated by the trading community.

Dynamic Smoothing

The unique dynamic smoothing feature calculates a smoothing factor based on the ratio of minutes between the Higher Time Frame (HTF) and your current time frame. This provides a sleek and responsive oscillator line that still holds the weight of the longer trend. One of the significant advantages of this feature is user experience; when you change your time frame, the HTF-values in your settings will remain consistent. This ensures that you can easily switch between different time frames without losing the insights provided by your selected HTF.

Visual Aids

Visual cues are an essential part of any trading strategy. The indicator not only plots signals to mark overbought and oversold conditions based on the dynamically smoothed oscillator but also provides you with the flexibility to customize your visual experience. You have the option to toggle on/off the display of these signals depending on your specific needs. Additionally, bands can be displayed at overbought and oversold levels, along with a reference middle line. If you switch between different oscillators (available in the parameter settings), remember to manually adjust the bands in the input settings to ensure signals matches with the type of oscillator to your liking.

User-Friendly Settings

We've grouped related settings together, making it easier for you to find what you're looking for. Adjust the oscillator type, length of bars, smoothing settings, and more with just a few clicks.

Information Table

A standout feature of this indicator is the real-time information table, which displays the values of all selected oscillators based on your specified Higher Time Frame (HTF) settings. This can be particularly useful for traders who depend on multiple indicators for their decision-making process. The data presented in the table is synchronized with the HTF options you've configured in the input settings, allowing for a more efficient and quick scan of values from higher time frames.

Educational Corner: The Power of the Information Table and Customization

The table incorporated into this indicator isn't just eye-candy; it's a practical tool designed to elevate your trading strategy. It dynamically displays real-time values of various oscillators for the HTF you've chosen. This is an exemplary use of TradingView's scripting capabilities to blend multiple indicators into a single visual panel, streamlining your analysis and decision-making process.

But here's the best part: You're not limited to what we've created. With some basic understanding of TradingView's scripting language, Pine Script, you can easily adapt this table to include different indicators that suit your unique trading style. The logic in the script is modular and can serve as a foundation for your own customized trading dashboard. So, go ahead, get creative and explore new combinations of indicators that will help you excel in your trading endeavors!

You no longer have to toggle between different charts or indicators to get the information you need; it's all there in one neatly organized table. We encourage you to tap into this feature and make it your own, empowering your trading like never before.

By doing so, you not only gain a more comprehensive toolset, but you also engage more deeply with your trading strategy, understanding its nuances and, ultimately, making more informed decisions.

Conclusion

The HTF Oscillators with Dynamic Smoothing is a versatile and powerful tool that brings together the best of both worlds: the perspective of higher time frames and the granularity of shorter ones. Its feature-rich setting options and real-time information table make it a potential useful addition to your trading toolkit.

Remember, while this indicator offers a comprehensive and smarter way to look at the markets, it is not a foolproof method for predicting market movements. Always use it in conjunction with other analysis methods and risk management strategies.

Buy/Sell EMA CandleThis indicator is designed to display various technical indicators, candle patterns, and trend directions on a price chart. Let's break down the code and explain its different sections:

Exponential Moving Averages (EMA):

The code calculates and plots five EMAs of different lengths (13, 21, 55, 90, and 200) on the price chart. These EMAs are used to identify trends and potential crossovers.

Engulfing Candle Patterns:

The code identifies and highlights potential bullish and bearish engulfing candle patterns. It checks if the current candle's body size is larger than the combined body sizes of the previous and subsequent four candles. If this condition is met, it marks the pattern on the chart.

s3.tradingview.com

EMA Crossovers:

The code identifies and highlights points where the shorter EMA (ema1) crosses above or below the longer EMA (ema2). It plots circles to indicate these crossover points.

Candle Direction and RSI Trend:

The code determines the trend direction of the last candle based on whether it closed higher or lower than its open price. It also calculates the RSI (Relative Strength Index) and determines its trend direction (overbought, oversold, or neutral) based on predefined thresholds.

s3.tradingview.com

Table Display:

The code creates a table displaying trend directions for different timeframes (monthly, weekly, daily, 4-hour, and 1-hour) for candle direction and RSI trends. The trends are labeled with "L" for long, "S" for short, and "N/A" for not applicable.

High Volume Bars (HVB):

The code identifies and colors bars with above-average volume as either bullish or bearish based on whether the price closed higher or lower than it opened. The color and conditions for high volume bars can be customized.

s3.tradingview.com

Doji Candle Pattern:

The code identifies and marks doji candle patterns, where the open and close prices are very close to each other within a certain percentage of the candle's high-low range.

RSI-Based Candle Coloring:

The code adjusts the color of the candles based on the RSI value. If the RSI value is above the overbought threshold or below the oversold threshold, the candles are colored yellow.

Usage and Interpretation:

Traders can use this indicator to identify potential trend changes based on EMA crossovers and candle patterns like engulfing and doji.

The RSI trend direction can provide additional insight into potential overbought or oversold conditions.

High volume bars can indicate potential price reversals or continuation patterns.

The table provides an overview of trend directions on different timeframes for both candle direction and RSI trends.

Keep in mind that this is a complex indicator with multiple features. Users should carefully evaluate its performance and consider combining it with other indicators and analysis methods for more accurate trading decisions.

The table is designed to provide a consolidated view of trend directions and other indicators across multiple timeframes. It is displayed on the chart and organized into rows and columns. Each row corresponds to a specific aspect of analysis, and each column corresponds to a different timeframe.

Here's a breakdown of the components of the table:

Row 1: Separation.

Row 2 (Header Row): This row contains the headers for the columns. The headers represent the different timeframes being analyzed, such as Monthly (M), Weekly (W), Daily (D), 4-hour (4h), and 1-hour (1h).

Row 3 (Content Row): This row contains labels indicating the types of information being displayed in the columns. The labels include "T" for Trend, "C" for Current Candle, and "R" for RSI Trend.

Row 4 and Onwards: These rows display the actual data for each aspect of analysis across different timeframes.

For each aspect of analysis (Trend, Current Candle, RSI Trend), the corresponding rows display the following information:

Monthly (M): The trend direction for the given aspect on the monthly timeframe.

Weekly (W): The trend direction for the given aspect on the weekly timeframe.

Daily (D): The trend direction for the given aspect on the daily timeframe.

4-hour (4h): The trend direction for the given aspect on the 4-hour timeframe.

1-hour (1h): The trend direction for the given aspect on the 1-hour timeframe.

The trend directions are represented by labels such as "L" for Long, "S" for Short, or "N/A" for Not Applicable.

The table's purpose is to provide a quick overview of trend directions and related information across multiple timeframes, aiding traders in making informed decisions based on the analysis of trend changes and other indicators.

Market Structure & Liquidity: CHoCHs+Nested Pivots+FVGs+Sweeps//Purpose:

This indicator combines several tools to help traders track and interpret price action/market structure; It can be divided into 4 parts;

1. CHoCHs, 2. Nested Pivot highs & lows, 3. Grade sweeps, 4. FVGs.

This gives the trader a toolkit for determining market structure and shifts in market structure to help determine a bull or bear bias, whether it be short-term, med-term or long-term.

This indicator also helps traders in determining liquidity targets: wether they be voids/gaps (FVGS) or old highs/lows+ typical sweep distances.

Finally, the incorporation of HTF CHoCH levels printing on your LTF chart helps keep the bigger picture in mind and tells traders at a glance if they're above of below Custom HTF CHoCH up or CHoCH down (these HTF CHoCHs can be anything from Hourly up to Monthly).

//Nomenclature:

CHoCH = Change of Character

STH/STL = short-term high or low

MTH/MTL = medium-term high or low

LTH/LTL = long-term high or low

FVG = Fair value gap

CE = consequent encroachement (the midline of a FVG)

~~~ The Four components of this indicator ~~~

1. CHoCHs:

•Best demonstrated in the below charts. This was a method taught to me by @Icecold_crypto. Once a 3 bar fractal pivot gets broken, we count backwards the consecutive higher lows or lower highs, then identify the CHoCH as the opposite end of the candle which ended the consecutive backwards count. This CHoCH (UP or DOWN) then becomes a level to watch, if price passes through it in earnest a trader would consider shifting their bias as market structure is deemed to have shifted.

•HTF CHoCHs: Option to print Higher time frame chochs (default on) of user input HTF. This prints only the last UP choch and only the last DOWN choch from the input HTF. Solid line by default so as to distinguish from local/chart-time CHoCHs. Can be any Higher timeframe you like.

•Show on table: toggle on show table(above/below) option to show in table cells (top right): is price above the latest HTF UP choch, or is price below HTF DOWN choch (or is it sat between the two, in a state of 'uncertainty').

•Most recent CHoCHs which have not been met by price will extend 10 bars into the future.

• USER INPUTS: overall setting: SHOW CHOCHS | Set bars lookback number to limit historical Chochs. Set Live CHoCHs number to control the number of active recent chochs unmet by price. Toggle shrink chochs once hit to declutter chart and minimize old chochs to their origin bars. Set Multi-timeframe color override : to make Color choices auto-set to your preference color for each of 1m, 5m, 15m, H, 4H, D, W, M (where up and down are same color, but 'up' icon for up chochs and down icon for down chochs remain printing as normal)

2. Nested Pivot Highs & Lows; aka 'Pivot Highs & Lows (ST/MT/LT)'

•Based on a seperate, longer lookback/lookforward pivot calculation. Identifies Pivot highs and lows with a 'spikeyness' filter (filtering out weak/rounded/unimpressive Pivot highs/lows)

•by 'nested' I mean that the pivot highs are graded based on whether a pivot high sits between two lower pivot highs or vice versa.

--for example: STH = normal pivot. MTH is pivot high with a lower STH on either side. LTH is a pivot high with a lower MTH on either side. Same applies to pivot lows (STL/MTL/LTL)

•This is a useful way to measure the significance of a high or low. Both in terms of how much it might be typically swept by (see later) and what it would imply for HTF bias were we to break through it in earnest (more than just a sweep).

• USER INPUTS: overall setting: show pivot highs & lows | Bars lookback (historical pivots to show) | Pivots: lookback/lookforward length (determines the scale of your pivot highs/lows) | toggle on/off Apply 'Spikeyness' filter (filters out smooth/unimpressive pivot highs/lows). Set Spikeyness index (determines the strength of this filter if turned on) | Individually toggle on each of STH, MTH, LTH, STL, MTL, LTL along with their label text type , and size . Toggle on/off line for each of these Pivot highs/lows. | Set label spacer (atr multiples above / below) | set line style and line width

3. Grade Sweeps:

•These are directly related to the nested pivots described above. Most assets will have a typical sweep distance. I've added some of my expected sweeps for various assets in the indicator tooltips.

--i.e. Eur/Usd 10-20-30 pips is a typical 'grade' sweep. S&P HKEX:5 - HKEX:10 is a typical grade sweep.

•Each of the ST/MT/LT pivot highs and lows have optional user defined grade sweep boxes which paint above until filled (or user option for historical filled boxes to remain).

•Numbers entered into sweep input boxes are auto converted into appropriate units (i.e. pips for FX, $ or 'handles' for indices, $ for Crypto. Very low $ units can be input for low unit value crypto altcoins.

• USER INPUTS: overall setting: Show sweep boxes | individually select colors of each of STH, MTH, LTH, STL, MTL, LTL sweep boxes. | Set Grade sweep ($/pips) number for each of ST, MT, LT. This auto converts between pips and $ (i.e. FX vs Indices/Crypto). Can be a float as small or large as you like ($0.000001 to HKEX:1000 ). | Set box text position (horizontal & vertical) and size , and color . | Set Box width (bars) (for non extended/ non-auto-terminating at price boxes). | toggle on/off Extend boxes/lines right . | Toggle on/off Shrink Grade sweeps on fill (they will disappear in realtime when filled/passed through)

4. FVGs:

•Fair Value gaps. Represent 'naked' candle bodies where the wicks to either side do not meet, forming a 'gap' of sorts which has a tendency to fill, or at least to fill to midline (CE).

•These are ICT concepts. 'UP' FVGS are known as BISIs (Buyside imbalance, sellside inefficiency); 'DOWN' FVGs are known as SIBIs (Sellside imbalance, buyside inefficiency).

• USER INPUTS: overall setting: show FVGs | Bars lookback (history). | Choose to display: 'UP' FVGs (BISI) and/or 'DOWN FVGs (SIBI) . Choose to display the midline: CE , the color and the line style . Choose threshold: use CE (as opposed to Full Fill) |toggle on/off Shrink FVG on fill (CE hit or Full fill) (declutter chart/see backtesting history)

////••Alerts (general notes & cautionary notes)::

•Alerts are optional for most of the levels printed by this indicator. Set them via the three dots on indicator status line.

•Due to dynamic repainting of levels, alerts should be used with caution. Best use these alerts either for Higher time frame levels, or when closely monitoring price.

--E.g. You may set an alert for down-fill of the latest FVG below; but price will keep marching up; form a newer/higher FVG, and the alert will trigger on THAT FVG being down-filled (not the original)

•Available Alerts:

-FVG(BISI) cross above threshold(CE or full-fill; user choice). Same with FVG(SIBI).

-HTF last CHoCH down, cross below | HTF last CHoCH up, cross above.

-last CHoCH down, cross below | last CHoCH up, cross above.

-LTH cross above, MTH cross above, STH cross above | LTL cross below, MTL cross below, STL cross below.

////••Formatting (general)::

•all table text color is set from the 'Pivot highs & Lows (ST, MT, LT)' section (for those of you who prefer black backgrounds).

•User choice of Line-style, line color, line width. Same with Boxes. Icon choice for chochs. Char or label text choices for ST/MT/LT pivot highs & lows.

////••User Inputs (general):

•Each of the 4 components of this indicator can be easily toggled on/off independently.

•Quite a lot of options and toggle boxes, as described in full above. Please take your time and read through all the tooltips (hover over '!' icon) to get an idea of formatting options.

•Several Lookback periods defined in bars to control how much history is shown for each of the 4 components of this indicator.

•'Shrink on fill' settings on FVGs and CHoCHs: Basically a way to declutter chart; toggle on/off depending on if you're backtesting or reading live price action.

•Table Display: applies to ST/MT/LT pivot highs and to HTF CHoCHs; Toggle table on or off (in part or in full)

////••Credits:

•Credit to ICT (Inner Circle Trader) for some of the concepts used in this indicator (FVGS & CEs; Grade sweeps).

•Credit to @Icecold_crypto for the specific and novel concept of identifying CHoCHs in a simple, objective and effective manner (as demonstrated in the 1st chart below).

CHoCH demo page 1: shifting tweak; arrow diagrams to demonstrate how CHoCHs are defined:

CHoCH demo page 2: Simplified view; short lookback history; few CHoCHs, demo of 'latest' choch being extended into the future by 10 bars:

USAGE: Bitcoin Hourly using HTF daily CHoCHs:

USAGE-2: Cotton Futures (CT1!) 2hr. Painting a rather bullish picture. Above HTF UP CHoCH, Local CHoCHs show bullish order flow, Nice targets above (MTH/LTH + grade sweeps):

Full Demo; 5min chart; CHoCHs, Short term pivot highs/lows, grade sweeps, FVGs:

Full Demo, Eur/Usd 15m: STH, MTH, LTH grade sweeps, CHoCHs, Usage for finding bias (part A):

Full Demo, Eur/Usd 15m: STH, MTH, LTH grade sweeps, CHoCHs, Usage for finding bias, 3hrs later (part B):

Realtime Vs Backtesting(A): btc/usd 15m; FVGs and CHoCHs: shrink on fill, once filled they repaint discreetly on their origin bar only. Realtime (Shrink on fill, declutter chart):

Realtime Vs Backtesting(B): btc/usd 15m; FVGs and CHoCHs: DON'T shrink on fill; they extend to the point where price crosses them, and fix/paint there. Backtesting (seeing historical behaviour):

Peer Performance - NIFTY36STOCKSI have created a peer performance dashboard for:

36 stocks from:

5 sectors of Nifty 100

This kind of dashboard is very useful for traders when they are planing to trade in a stocks and like to see how that is stocks is performing against other stocks in the same sector . Picking outperforming stocks will always give outstanding results when market starts moving. os having view on teh complete sector will always be good for traders before picking a specific stock.

Sectors covered in this indicators are:

Indian Auto Sector

Banking Sector

Oil, Gas and Energy Stocks

Cement Sector

Technology Sector

It will help traders reviewing performance ( stock return in last 1 year) of group of stocks from a particular sector .

Basically 5 functions are used to plot this dashboard

using "if " function to shortlist the stocks and the sector it belongs to.

tablo function to plot a table with specific parameters like number of row and columns, color of the frame of table

Getting yearly return into a series of variables using "request.security" function

str.tostring function is used to convert yearly return into a series of text so that it can inserted into the table cell.

finally plotting all the text and yearly return values using table.cell function

Zendog V2 backtest DCA bot 3commasHi everyone,

After a few iterations and additional implemented features this version of the Backtester is now open source.

The Strategy is a Backtester for 3commas DCA bots. The main usage scenario is to plugin your external indicator, and backtest it using different DCA settings.

Before using this script please make sure you read these explanations and make sure you understand how it works.

Features:

- Because of Tradingview limitations on how orders are grouped into Trades, this Strategy statistics are calculated by the script, so please ignore the Strategy Tester statistics completely

Statistics Table explained:

- Status: either all deals are closed or there is a deal still running, in which case additional info

is provided below, as when the deal started, current PnL, current SO

- Finished deals: Total number of closed deals both Winning and Losing.

A deal is comprised as the Base Order (BO) + all Safety Orders (SO) related to that deal, so this number

will be different than the Strategy Tester List of Trades

- Winning Deals: Deal ended in profit

- Losing deals: Deals ended with loss due to Stop Loss. In the future I might add a Deal Stop condition to

the script, so that will count towards this number as well.

- Total days ( Max / Avg days in Deal ):

Total Days in the Backtest given by either Tradingview limitation on the number of candles or by the

config of the script regarding "Limit Date Range".

Max Days spent in a deal + which period this happened.

Avg days spent in a deal.

- Required capital: This is the total capital required to run the Backtester and it is automatically calculated by

the script taking into consideration BO size, SO size, SO volume scale. This should be the same as 3commas.

This number overwrites strategy.initial_capital and is used to calculate Profit and other stats, so you don't need

to update strategy.initial_capital every time you change BO/SO settings

- Profit after commission

- Buy and Hold return: The PnL that could have been obtained by buying at the close of the first candle of the

backtester and selling at the last.

- Covered deviation: The % of price move from initial BO order covered by SO settings

- Max Deviation: Biggest market % price move vs BO price, in the other direction (for long

is down, for short it is up)

- Max Drawdown: Biggest market % price move vs Avg price of the whole Trade (BO + any SO), in the other

direction (for long price goes down, for short it goes up)

This is calculated for the whole Trade so it is different than List of Trades

- Max / Avg bars in deal

- Total volume / Commission calculated by the strategy. For correct commission please set Commission in the

Inputs Tab and you may ignore Properties Tab

- Close stats for deals: This is a list of how many Trades were closed at each step, including Stop Loss (if

configured), together with covered deviation for that step, the number of deals, and the percentage of this

number from all the deals

TODO: Might add deal avg value for each step

- Settings Table that can be enabled / disabled just to have an overview of your configs on the chart, this is a

drawn on bottom left

- Steps Table similar to 3commas, this is also drawn on bottom left, so please disable Settings table if you want

to see this one

TODO: Might add extra stats here

- Deal start condition: built in RSI-7 or plugin any external indicator and compare with any value the indicator plots

(main purpose of this strategy is to connect your own studies, so using external indicator is recommended)

- Base order and safety orders configs similar to 3commas (order size, percent deviation, safety orders,

percent scale and volume scale)

- Long and Short

- Stop Loss

- Support for Take profit from base order or from Total volume of the deal

- Configs help (besides self explanatory):

- Chart theme: Adjust according to the theme you run on. There is no way to detect theme at the moment.

This adjust different colors

- Deal Start Type: Either a builtin RSI7 or "External indicator"

- Indicator Source an value: If using External Indicator then select source, comparison and value.

For example you could start a deal when Volume is greater than xxxx, or code a custom indicator that plots

different values based on your conditions and test those values

- Visuals / Decimals for display: Adjust according to your symbol

- BO Entry Price for steps table: This is the BO start deal price used to calculate the steps in the table

chanlun缠论 - 笔与中枢Overview

The Chanlun (缠论) Strokes & Central Zones indicator is an advanced technical analysis tool based on Chinese Chan Theory (Chanlun Theory). It automatically identifies market structure through "strokes" (笔) and "central hubs" (中枢), providing traders with a systematic framework for understanding price movements, trend structure, and potential reversal zones.

Theoretical Foundation

Chan Theory is a sophisticated price action methodology that breaks down market movements into hierarchical structures:

Local Extremes: Swing highs and lows identified through lookback periods

Strokes (笔): Valid price movements between opposite extremes that meet specific criteria

Central Hubs (中枢): Consolidation zones formed by overlapping strokes, representing key support/resistance areas

Key Components

1. Local Extreme Detection

Identifies swing highs and lows using a configurable lookback period (default: 5 bars)

Only considers extremes within the specified calculation range

Forms the foundation for stroke construction

2. Stroke (笔) Identification

The indicator applies a multi-stage filtering process to identify valid strokes:

Stage 1 - Extreme Consolidation:

Merges consecutive extremes of the same type (high or low)

Keeps only the most extreme value (highest high or lowest low)

Stage 2 - Stroke Validation:

Ensures minimum bar gap between strokes (default: 4 bars)

Alternative validation: 2+ bars with >1% price change

Eliminates noise and insignificant price movements

Color Coding:

White Lines: Regular up/down strokes

Yellow Lines: Strokes that form part of a central hub

Customizable width and colors for different stroke types

3. Central Hub (中枢) Formation

A central hub forms when at least 3 consecutive strokes have overlapping price ranges:

Formation Rules:

Stroke 1:

Stroke 2:

Stroke 3:

Hub Upper = MIN(High1, High2, High3)

Hub Lower = MAX(Low1, Low2, Low3)

Valid if: Hub Upper > Hub Lower

Hub Extension:

Subsequent strokes that overlap with the hub extend it

Hub ends when a stroke no longer overlaps

Creates rectangular zones on the chart

Visual Representation:

Green rectangular boxes: Mark the time and price range of each central hub

Dashed extension lines: Show the latest hub boundaries extending to the right

Price labels on axis: Display exact hub upper and lower boundary values

4. Extreme Point Markers (Optional)

Red markers for tops (▼)

Green markers for bottoms (▲)

Marks every validated stroke extreme point

Useful for detailed structure analysis

5. Information Table (Optional)

Displays real-time statistics:

Symbol name

Current timeframe

Lookback period setting

Minimum gap setting

Total stroke count

Parameter Settings

Performance Settings

Max Bars to Calculate (3600): Limits historical calculation to improve performance

Local Extreme Lookback Period (5): Bars used to identify swing highs/lows

Min Gap Bars (4): Minimum bars required between valid strokes

Display Settings

Show Strokes: Toggle stroke line visibility

Show Central Hub: Toggle hub box visibility

Show Hub Extension Lines: Toggle dashed boundary lines

Show Extreme Point Marks: Toggle top/bottom markers

Show Info Table: Toggle statistics table

Color Settings

Full customization of:

Up/down stroke colors and widths

Hub stroke colors and widths

Hub border and background colors

Extension line colors

Trading Applications

Trend Structure Analysis

Uptrend: Series of higher highs and higher lows connected by strokes

Downtrend: Series of lower highs and lower lows connected by strokes

Consolidation: Formation of central hubs indicating range-bound movement

Support and Resistance Identification

Central Hub Zones: Act as strong support/resistance areas

Hub Upper Boundary: Resistance level in consolidation, support after breakout

Hub Lower Boundary: Support level in consolidation, resistance after breakdown

Price tends to react at these levels due to market structure memory

Breakout Trading

Bullish Breakout: Price closes above hub upper boundary

Previous resistance becomes support

Entry on retest of upper boundary

Stop loss below hub zone

Bearish Breakdown: Price closes below hub lower boundary

Previous support becomes resistance

Entry on retest of lower boundary

Stop loss above hub zone

Reversal Detection

Hub Formation After Trend: Signals potential trend exhaustion

Multiple Hub Levels: Create probability zones for reversals

Stroke Count: Excessive strokes within hub suggest weakening momentum

Position Management

Use hub boundaries for stop loss placement

Scale out positions at hub edges

Re-enter on retests of broken hub levels

Interpretation Guide

Strong Trending Market

Long, clear strokes with minimal overlap

Few or no central hubs forming

Strokes consistently in same direction

Wide spacing between extremes

Consolidating Market

Multiple central hubs forming

Short, overlapping strokes

Yellow hub strokes dominate the chart

Narrow price range

Trend Transition

Hub formation after extended trend

Stroke direction changes frequently

Hub boundaries being tested repeatedly

Potential reversal zone

Advanced Usage Techniques

Multi-Timeframe Analysis

Higher Timeframe: Identify major hub zones for overall market structure

Lower Timeframe: Find precise entry points within larger structure

Alignment: Trade when lower timeframe strokes align with higher timeframe hub breaks

Hub Quality Assessment

Wide Hubs: Strong consolidation, higher probability support/resistance

Narrow Hubs: Weak consolidation, may break easily

Extended Hubs: More strokes = stronger zone

Isolated Hubs: Single hub = potential pivot point

Stroke Analysis

Stroke Length: Longer strokes = stronger momentum

Stroke Speed: Fewer bars per stroke = explosive moves

Stroke Clustering: Many short strokes = indecision

Best Practices

Parameter Optimization

Adjust lookback period based on timeframe and volatility

Lower periods (3-4): More strokes, more noise, faster signals

Higher periods (7-10): Fewer strokes, cleaner structure, slower signals

Confirmation Strategy

Don't trade on strokes alone

Combine with volume analysis

Use candlestick patterns at hub boundaries

Wait for breakout confirmation

Risk Management

Always place stops outside hub zones

Use hub width to size positions (wider hub = smaller position)

Exit if price re-enters broken hub from wrong direction

Avoid Common Pitfalls

Don't trade within central hubs (range-bound, unpredictable)

Don't ignore higher timeframe hub structures

Don't chase strokes after they've extended far from hub

Don't trust single-stroke hubs (need 3+ strokes for validity)

Performance Considerations

Max Bars Limit: Set to 3600 to balance detail with performance

Safe Distance Calculation: Only draws objects within 2000 bars of current price

Object Cleanup: Automatically removes old drawing objects to prevent memory issues

Efficient Arrays: Uses indexed arrays for fast lookup and processing

Ideal Market Conditions

Best Performance:

Liquid markets with clear structure (major forex pairs, indices, large-cap stocks)

Trending markets with periodic consolidations

Medium to high volatility for clear stroke formation

Less Effective:

Extremely choppy, directionless markets

Very low timeframes (< 5 minutes) with excessive noise

Illiquid instruments with erratic price action

Integration with Other Indicators

Complementary Tools:

Volume Profile: Confirm hub significance with volume nodes

Moving Averages: Use for trend bias within stroke structure

RSI/MACD: Momentum confirmation at hub boundaries

Fibonacci Retracements: Hub levels often align with Fib levels

Advantages

✓ Objective Structure: Removes subjectivity from market structure analysis

✓ Visual Clarity: Color-coded strokes and clear hub zones

✓ Multi-Timeframe Applicable: Works on all timeframes from minutes to months

✓ Complete Framework: Provides entry, exit, and risk management levels

✓ Theoretical Foundation: Based on proven Chan Theory methodology

✓ Customizable: Extensive parameter and visual customization options

Limitations

⚠ Learning Curve: Requires understanding of Chan Theory principles

⚠ Lag Factor: Strokes confirm after price movements complete

⚠ Parameter Sensitivity: Different settings produce significantly different results

⚠ Choppy Market Struggles: Can generate excessive hubs in range-bound conditions

⚠ Computation Intensive: May slow down on lower-end systems with max bars setting

Optimization Tips

Timeframe Selection

Scalping: 5-15 minute charts, lookback period 3-4

Day Trading: 15-60 minute charts, lookback period 4-5

Swing Trading: 4-hour to daily charts, lookback period 5-7

Position Trading: Daily to weekly charts, lookback period 7-10

Volatility Adjustment

High volatility: Increase minimum gap bars to reduce noise

Low volatility: Decrease lookback period to capture smaller moves

Visual Optimization

Use contrasting colors for different market conditions

Adjust line widths based on chart resolution

Toggle markers off for cleaner appearance once familiar with structure

Quick Start Guide

For Beginners:

Start with default settings (5 lookback, 4 min gap)

Enable "Show Info Table" to track stroke count

Focus on identifying clear hub formations

Practice waiting for price to break hub boundaries before trading

For Advanced Users:

Optimize lookback and gap parameters for your instrument

Use hub strokes (yellow) to identify key consolidation zones

Combine with multiple timeframes for confirmation

Develop entry rules based on hub breakout/retest patterns

This indicator provides a complete structural framework for understanding market behavior through the lens of Chan Theory, offering traders a systematic approach to identifying high-probability trading opportunities.

BullTrader - ParabolicSARFlipSignals(NonRepainting)TP/SL🧠 Purpose & Concept

This indicator refines Wilder’s Parabolic SAR into a simple, non‑repainting alert and visualization system that marks each confirmed trend flip with a clear buy or sell signal.

It also auto‑generates dynamic, ATR‑based Take‑Profit (TP) and Stop‑Loss (SL) levels, keeps them updating with price in real time, and displays the current market bias in an on‑chart table.

The goal: clarity and automation without complexity — see exactly when a new bullish or bearish phase begins, what your current TP/SL targets are, and receive a single clean alert for every new flip.

⚙️ How It Works

1. The built‑in ta.sar() function tracks the Parabolic SAR dots.

2. When a candle closes across the SAR line, a trend‑change is confirmed:

• Price crossing above a SAR dot → Buy Flip (green triangle).

• Price crossing below a SAR dot → Sell Flip (red triangle).

3. On each flip, the indicator calculates dynamic ATR‑based TP / SL targets:

TP = entry ± (ATR × tpMult) and SL = entry ∓ (ATR × slMult)

These values move automatically as the trend develops.

4. A small floating label beside the latest bar shows live‑updated TP / SL numbers.

5. A color‑coded table in the upper‑right corner displays the current trend: Lime = Bullish, Red = Bearish, Yellow = Neutral.

6. Each new flip triggers an easy‑to‑use Buy / Sell alert after the bar closes—no repainting.

🔔 Alerts

Alert Name Triggers When Message

SAR Buy Flip Alert Green triangle (bullish reversal) “BUY Flip — Parabolic SAR on {{ticker}} ({{interval}})”

SAR Sell Flip Alert Red triangle (bearish reversal) “SELL Flip — Parabolic SAR on {{ticker}} ({{interval}})”

📈 Chart Elements

Element Meaning

🟠 Orange cross Standard Parabolic SAR trail.

🟢 / 🔴 Triangles Confirmed buy / sell flips (non‑repainting).

Bright lime/red TP‑SL box Live ATR targets that move with price.

Trend table (top‑right) Instant status of bullish/bearish bias.

✅ Features & Highlights

Non‑repainting — all signals confirm on closed bars.

Visual clarity — single pair of bright triangles for flips.

Dynamic ATR‑based TP / SL values that auto‑trail with trend.

Always‑visible trend summary table.

Two ready‑made alert types (Buy / Sell).

Lightweight and optimized for any timeframe or symbol.

💡 Best Use

Ideal for traders who prefer clean trend‑based entries and volatility‑adaptive exits without signal clutter:

Pair it with your existing strategy or use it standalone for reversal‑based swing and intraday trading.

Period Range AnalyzerThis indicator analyzes a specific periodic range, which can start from a fixed date or a defined lookback period. It draws percentage levels and colored zones between the highest and lowest price. It also displays a detailed information table, which shows the price's position within the range in "Trend" mode, and the relative strength of currency pairs in "Forex" mode. The current price position is also indicated by a label with a percentage value and the name of the corresponding zone.

User Guide

Calculation Method

This setting determines how the indicator defines the range used for the calculation.

Lookback Period: In this mode, the indicator uses the last N candles (the number can be specified in the "Lookback Period (bars)" field). The range (the highest and lowest price) is "floating," meaning it is recalculated with each new candle based on the last N candles.

Date Based: In this mode, the calculation starts from a fixed date and time you select. The indicator finds the opening price of the start date and continuously tracks the highest and lowest price from that point on. This mode is ideal for measuring performance from a specific event (e.g., start of a week/month/year, news).

Data Handling Note: If you select a date in "Date Based" mode for which no data is available on the current timeframe (e.g., switching to a very low timeframe), the indicator will automatically use the earliest available candle as the starting point. All calculations (Open, Max, Min, Range, Percentage, Change, Trend) are based on this actual start date.

Start Date & Time

This setting is only active in "Date Based" mode.

Here you can specify the fixed starting point for the calculation.

The specified time is in the Exchange timezone.

Important limitation: Due to TradingView platform limits, visual elements (levels, zones) are only drawn for a maximum of 250 candles back. If the set date is older than this, the calculation still applies to the entire period (from the set date), but the drawing only covers the last 250 candles. The table always displays accurate data for the entire period.

When switching to a higher timeframe, the range may restart from a slightly later bar due to TradingView's bar alignment. For best accuracy, set your timeframe first, then select the start date.

Table Mode

This setting controls what data the information table displays.

Trend: This is the default mode, which works on any symbol (stock, index, crypto, etc.). It displays information related to the trend and the range.

Forex: This is a special mode used to measure the strength of currency and crypto pairs. It only works on symbols with exactly 6 characters (e.g., "EURUSD", "BTCUSD"). It treats the first 3 characters as the base currency (e.g., EUR) and the last 3 as the quote currency (e.g., USD). If the symbol does not have 6 characters, the table will automatically display in "Trend" mode.

Trend

This trend determination operates based on the formation order of the high and low within the analyzed range:

Its switch is located in the “Table Additional Rows” menu.

Bullish: Indicated if the low was formed before the high (on different candles). Or if they formed on the same candle, it was a bullish candle.

Bearish: Indicated if the high was formed before the low (on different candles). Or if they formed on the same candle, it was a bearish candle.

Neutral: Indicated if the high and low formed on the same candle, and it was a "doji" candle (close = open).

Upper & Lower Threshold

These settings (Upper Threshold (%) and Lower Threshold (%) in the "Label Coloring" section) primarily determine the state (Bullish/Bearish/Neutral) of the top row of the table.

The logic is not based on the percentage change of the price movement, but on the current price's position within the range, where the bottom of the range is 0% and the top is 100%.

Upper Threshold (%): The percentage level (e.g., 60.0) above which the indicator considers the price position "Bullish" (or "Strong").

Lower Threshold (%): The percentage level (e.g., 40.0) below which the indicator considers the price position "Bearish" (or "Weak").

If the price is between the two (e.g., between 40% and 60%), the signal is Neutral.

Secondary function: These thresholds also control the color of the label next to the price, provided the "Dynamic Label Coloring" option is enabled.

Range Percentage Analyzer This indicator is a tool for analyzing the market range and trend. It calculates the extent of price movement between a specified starting point and the current price, displaying it as a percentage.

The calculation can be based on a fixed lookback period (e.g., the last 30 candles) or from a fixed start date. It also provides a clear table that shows the general trend in "Trend" mode, and the relative strength of the base and quote currencies of forex pairs (e.g., EURUSD) in "Forex" mode.

User Guide

Calculation Method

This setting determines how the indicator defines the starting point for the calculation.

Lookback Period: In this mode, the indicator uses the last N candles (the number can be specified in the "Lookback Period (bars)" field, maximum 250).

The starting point is "floating," meaning it shifts with each new candle. For example, with a setting of 30, the 30th candle from the current one will always be the starting point.

Date Based: In this mode, the calculation starts from a fixed date and time you select.

This mode is ideal for measuring performance from a specific event (e.g., news, start of a week/month).

Note: If you select a date in "Date Based" mode for which no data is available on the current timeframe (e.g., switching to a very low timeframe), the indicator will automatically use the earliest available candle as the starting point.

Start Date & Time

This setting is only active in "Date Based" mode.

Here you can specify the fixed starting point for the calculation.

The specified time is in the Exchange timezone.

Important limitation: Due to TradingView platform limits, visual elements (box, line) are only drawn for a maximum of 250 candles back.

If the set date is older than this, the calculation still applies to the entire period (from the set date), but the drawing only covers the last 250 candles.

When switching to a higher timeframe, the range may restart from a slightly later bar due to TradingView's bar alignment. For best accuracy, set your timeframe first, then select the start date.

Table Mode

This setting controls what data the information table displays.

Trend: This is the default mode, which works on any symbol (stock, index, crypto, etc.). It displays information related to the trend.

Forex: This is a special mode used to measure the strength of currency pairs.

It only works on symbols with exactly 6 characters (e.g., "EURUSD", "BTCUSD"). It treats the first 3 characters as the base currency (e.g., EUR) and the last 3 as the quote currency (e.g., USD).

If the symbol does not have 6 characters, the table will automatically display in "Trend" mode.

Extremes Trend Row

If this is enabled, the table displays an additional row that determines the trend based on the formation order of the high and low within the analyzed range.

The logic is as follows:

Bullish: Indicated if the low was formed before the high.

(Or if they formed on the same candle, which was a bullish candle).

Bearish: Indicated if the high was formed before the low.

(Or if they formed on the same candle, which was a bearish candle).

Neutral: Indicated if the high and low formed on the same candle, and it was a "doji" candle (close = open).

Upper & Lower Threshold

These settings control the logic for the "Change Trend" and "Forex Display" rows at the top of the table.

They determine when the total percentage change for the entire period is considered "Bullish/Strong", "Bearish/Weak", or "Neutral".

Upper Threshold (%): The percentage value (default 0.1%) above which the indicator considers the change "Bullish/Strong".

Lower Threshold (%): The percentage value (default -0.1%) below which the indicator considers the change "Bearish/Weak".

If the change is between the two, the signal is Neutral.

SECTOR ROTATION Sector Rotation Indicator with Auto Chart Symbol

This indicator helps traders track relative performance across multiple indices/sectors simultaneously, making it easy to identify sector rotation and market leadership.

Key Features:

✅ 21 Symbols Tracking: Monitor 20 customizable symbols + your current chart symbol automatically(DIVIDEND SYMBOL)

✅ Percentage Performance: All moving averages show percentage gain/loss from 1 timeframe period ago

✅ Color-Coded Visualization: Heat map coloring (red to green) based on relative performance ranking

✅ Flexible Timeframes: Works on any timeframe from 1-minute to 12-month charts

✅ Performance Table: Quick-view table showing candle performance with inside/outside bar detection

✅ Indian Market Ready: Pre-configured with NSE indices (NIFTY, BANKNIFTY, and sectoral indices)

Default Symbols (Customizable):

NIFTY, CNXSMALLCAP, CNXMIDCAP, BANKNIFTY

Sector indices: IT, AUTO, PHARMA, METAL, ENERGY, FMCG, etc.

Plus your current chart symbol (automatically added)

How It Works:

Select your preferred timeframe (1D, 1W, 1M, etc.)

The indicator calculates percentage performance from given period ago

Moving averages show smoothed performance trends

Colors indicate relative strength: Green = outperformers, Red = underperformers

Perfect For:

Sector rotation analysis

Relative strength comparison

Market breadth assessment

Index/ETF traders

Swing and position traders

Settings:

Adjustable MA length (default: 20)

Customizable colors and table position

Show/hide percentage labels

Horizontal or vertical table layout

This is not any buy or sell signal or recommendation, consult with your advisor first.

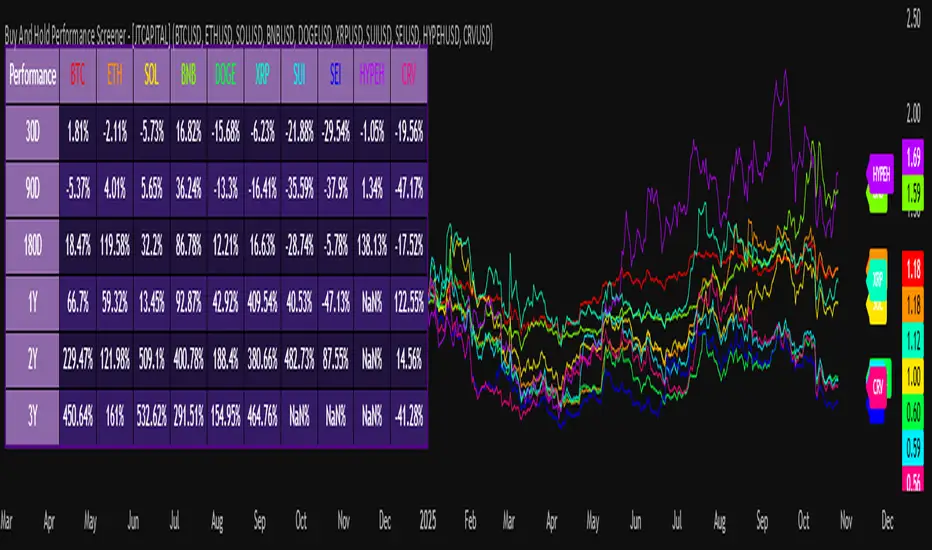

Buy And Hold Performance Screener - [JTCAPITAL]Buy And Hold Performance Screener – is a script designed to track and display multi-asset “buy and hold” performance curves and performance statistics over defined timeframes for selected symbols. It doesn’t attempt to time entries or exits; rather, it shows what would happen if one simply bought the asset at the defined start date and held it.

The indicator works by calculating in the following steps:

Start Date Definition

The script begins by reading an input for the start date. This defines the bar from which the equity curves begin.

Symbol Definitions & Close Price Retrieval

The script allows the user to specify up to ten tickers. For each ticker it uses request.security() on the “1D” timeframe to retrieve the daily close price of that symbol.

Plot Enable Inputs

For each ticker there is an input boolean controlling whether the equity curve for that ticker should be plotted.

Asset Name Cleaning

The helper function clean_name(string asset) => … takes the asset string (e.g., “CRYPTO:SOLUSD”) and manipulates it (via string splitting and replacements) to derive a cleaned short name (e.g., “SOL”). This name is used for visuals (labels, table headers).

Equity Curve Calculation (“HODL”)

The helper function f_HODL(closez) defines a variable equity that assumes a starting equity of 1 unit at the start date and then multiplies by the ratio of each bar’s close to the prior bar’s close: i.e. daily compounding of returns.

Performance Metrics Calculation

The helper function f_performance(closez) calculates, for each symbol’s close series, the percentage change of the current close relative to its close 30 days ago, 90 days ago, 180 days ago, 1 year ago (365 days), 2 years ago (730 days) and 3 years ago (1095 days).

Equity Curve Plots

For each ticker, if the corresponding plot input is true, the script assigns a plotted variable equal to the equity curve value. Its then drawing each selected equity curve on the chart, each in a distinct color.

Table Construction

If the plottable input is true, the script constructs a table and populates it with rows and column corresponding to the assigned tickers and the set 6 timeframes used for display.

Buy and Sell Conditions:

Since this is strictly a “buy-and-hold” performance screener, there are no explicit buy or sell signals generated or plotted. The script assumes: buy at the defined start_date, hold continuously to present. There are no filters, no exit logic, no take-profit or stop-loss. The benefit of this approach is to provide a clean benchmark of how selected assets would have performed if one simply adopted a passive “buy & hold” approach from a given start date.

Features and Parameters:

start_date (input.time) : Defines the date from which performance and equity curves begin.

ticker1 … ticker10 (input.symbol) : User-selectable asset symbols to include in the screener.

plot1 … plot10 (input.bool) : Boolean flags to enable/disable plotting of each asset’s equity curve.

plottable (input.bool) : Flag to enable/disable drawing the performance table.

Colored plotting + Labels for identifying each asset curve on the chart.

Specifications:

Here is a detailed breakdown of every calculation/variable/function used in the script and what each part means:

start_date

This is defined via input.time(timestamp("1 Jan 2025"), title = "Start Date"). It allows the user to pick a specific calendar date from which the equity curves and performance calculations will start.

ticker1 … ticker10

These inputs allow the user to select up to ten different assets (symbols) to monitor. The script uses each of these to fetch daily close prices.

plot1 … plot10

Boolean inputs controlling which of the ten asset equity curves are plotted. If plotX is true, the equity curve for ticker X will be visible; otherwise it will be not plotted. This gives the user flexibility to include or exclude specific assets on the chart.

Returns the cleaned asset short name.

This provides friendly text labels like “BTC”, “ETH”, “SOL”, etc., instead of full symbol codes.

The choice of distinct colours for each asset helps differentiate curves visually when multiple assets are overlaid.

Colour definitions

Variables color1…color10 are explicitly defined via color.rgb(r,g,b) to give each asset a unique colour (e.g., red, orange, yellow, green, cyan, blue, purple, pink, etc.).

What are the benefits of combining these calculations?

By computing equity curves for multiple assets from the same start date and overlaying them, you can visualise comparative performance of different assets under a uniform “buy & hold” assumption.

The performance table adds multi-horizon returns (30 D, 90 D, 180 D, 1 Y, 2 Y, 3 Y) which helps the user see both short-term and longer-term performance without having to manually compute returns.

The use of daily close data via request.security(..., "1D") removes dependency on the chart’s timeframe, thereby standardising the comparison across assets.

The equity curve and table together provide both visual (curve) and numerical (table) summaries of performance, making it easier to spot trends, divergences, and cross-asset comparisons at a glance.

Because it uses compounding (equity := equity * (closez / closez )), the curves reflect the real growth of a 1-unit investment held over time, rather than only simple returns.

The labelling of curves and the color-coding make the multi-asset overlay easier to interpret.

Using a clean start date ensures that all curves begin at the same point (1 unit at start_date), making relative performance intuitive.

Because of this, the script is useful as a benchmarking tool: rather than trying to pick entries or exit points, you can simply compare “what if I had held these assets since Jan 1 2025” (or your chosen date), and see which assets out-/under-performed in that period. It helps an investor or trader evaluate the long-term benefits of passive vs. active management, or of allocation decisions.

Please note:

The script assumes continuous daily data and does not account for dividends, fees, slippage, or tax implications.

It does not attempt to optimise timing or provide trading signals.

Returns prior to the start date are ignored (equity only begins once time >= start_date).

For newly listed assets with fewer than 365 or 730 or 1095 days of history, the longer-horizon returns may return na or misleading values.

Because it uses request.security() without specifying lookahead, and on “1D” timeframe, it complies with standard usage but you should verify there is no look-ahead bias in your particular setup.

ENJOY!

Multi-Timeframe EMA (5 Configurable)Here's a comprehensive description you can use for your indicator:

Multi-Timeframe EMA Indicator (5 Configurable Slots)

Description

This indicator displays up to 5 Exponential Moving Averages (EMAs) from different timeframes simultaneously on a single chart. Perfect for multi-timeframe analysis, it allows traders to visualize key EMAs from intraday to higher timeframes without switching charts.

Key Features

5 Independent EMA Slots: Each slot can be configured with its own timeframe, EMA length, and color

Flexible Configuration: Mix any timeframes and EMA lengths (e.g., 1m EMA 50, 15m EMA 200, 4h EMA 100)

Smart Label Formatting: Automatically displays timeframes in readable format (minutes, hours, or days)

Optional Data Table: Toggle a compact table showing EMA values and price distance percentages

Individual Toggle Controls: Enable/disable each EMA independently without losing settings

Customizable Styling: Adjust colors and line width to match your chart theme

Default Configuration

EMA 1: 1-minute timeframe, EMA 200 (Red)

EMA 2: 5-minute timeframe, EMA 200 (Purple)

EMA 3: 15-minute timeframe, EMA 200 (Yellow)

EMA 4: 1-hour timeframe, EMA 200 (Blue)

EMA 5: 4-hour timeframe, EMA 200 (Orange)

How to Use

Add the indicator to any chart

Configure each EMA slot in the settings:

Timeframe: Choose from 1m, 5m, 15m, 1h, 4h, D, W, M, or custom

Length: Set the EMA period (default 200)

Color: Select a color for easy identification

Enable "Show Line Labels" to see EMA identifiers on the right side

Enable "Show Values Table" for a detailed view of current values and distances

Use Cases

Trend Analysis: Identify alignment across multiple timeframes

Support/Resistance: Use higher timeframe EMAs as dynamic S/R levels

Entry/Exit Timing: Enter on lower timeframe signals near higher timeframe EMAs

Multi-Timeframe Confirmation: Validate setups when price is above/below key EMAs

Scalping: Monitor 1m/5m EMAs while respecting 1h/4h trend direction

Tips

All EMAs update in real-time and move with the chart

Use contrasting colors for easier visual distinction

Disable unused slots to declutter your chart

The table shows percentage distance from current price to each EMA

Works on any symbol and any chart timeframe

Material Color Palette Library█ OVERVIEW

Unlock a world of color in your Pine Script® projects with the Material Color Palette Library . This library provides a comprehensive and structured color system based on Google's Material Design palette, making it incredibly easy to create visually appealing and professional-looking indicators and strategies.

Forget about guessing hex codes. With this library, you have access to 19 distinct color families, each offering a wide range of shades. Every color can be fine-tuned with saturation, darkness, and opacity levels, giving you precise control over your script's appearance.

To make development even easier, the library includes a visual cheatsheet. Simply add the script to your chart to display a full table of all available colors and their corresponding parameters.

█ KEY FEATURES

Vast Spectrum: 19 distinct color families, from vibrant reds and blues to subtle greys and browns.

Fine-Tuned Control: Each color function accepts parameters for `saturationLevel` (1-13 or 1-9) and `darkLevel` (1-3) to select the perfect shade.

Opacity Parameter: Easily add transparency to any color for fills, backgrounds, or lines.

Quick Access Tones: A simple `tone()` function to grab base colors by name.

Visual Cheatsheet: An on-chart table displays the entire color palette, serving as a handy reference guide during development.

█ HOW TO USE

As a library, this script is meant to be imported into your own indicators or strategies.

1. Import the Library

Add the following line to the top of your script. Remember to replace `YourUsername` with your TradingView username.

import mastertop/ColorPalette/1 as colors

2. Call a Color Function

You can now use any of the exported functions to set colors for your plots, backgrounds, tables, and more.

The primary functions take three arguments: `functionName(saturationLevel, darkLevel, opacity)`

`saturationLevel`: An integer that controls the intensity of the color. Ranges from 1 (lightest) to 13 (most vibrant) for most colors, and 1-9 for `brown`, `grey`, and `blueGrey`.

`darkLevel`: An integer from 1 to 3 (1: light, 2: medium, 3: dark).

`opacity`: An integer from 0 (opaque) to 100 (invisible).

Example Usage:

Let's plot a moving average with a specific shade of teal.

// Import the library

import mastertop/ColorPalette/1 as colors

indicator("My Script with Custom Colors", overlay = true)

// Calculate a moving average

ma = ta.sma(close, 20)

// Plot the MA using a color from the library

// We'll use teal with saturation level 7, dark level 2, and 0% opacity

plot(ma, "MA", color = colors.teal(7, 2, 0), linewidth = 2)

3. Using the `tone()` Function

For quick access to a base color, you can use the `tone()` function.

// Set a red background with 85% transparency

bgcolor(colors.tone('red', 85))

█ VISUAL REFERENCE

To see all available colors at a glance, you can add this library script directly to your chart. It will display a comprehensive table showing every color variant. This makes it easy to pick the exact shade you need without guesswork.

This library is designed for fellow Pine Script® developers to streamline their workflow and enhance the visual quality of their scripts. Enjoy!

TradeVision Pro - Multi-Factor Analysis System═══════════════════════════════════════════════════════════════════

TRADEVISION PRO - MULTI-FACTOR ANALYSIS SYSTEM

Created by Zakaria Safri

═══════════════════════════════════════════════════════════════════

A comprehensive technical analysis tool combining multiple factors for

signal generation, trend analysis, and dynamic risk management visualization.

Designed for educational purposes to study multi-factor convergence trading

strategies across all markets and timeframes.

⚠️ IMPORTANT DISCLAIMER:

This indicator is provided for EDUCATIONAL and INFORMATIONAL purposes only.

It does NOT constitute financial advice, investment advice, or trading advice.

Past performance does not guarantee future results. Trading involves

substantial risk of loss. Always do your own research and consult a

financial advisor before making trading decisions.

🎯 KEY FEATURES

═══════════════════════════════════════════════════════════════════

✅ MULTI-FACTOR SIGNAL GENERATION

• Price Volume Trend (PVT) analysis

• Rate of Change (ROC) momentum confirmation

• Volume-Weighted Moving Average (VWMA) trend filter

• Simple Moving Average (SMA) price smoothing

• Signals only when all factors align

✅ DYNAMIC RISK VISUALIZATION (Educational Only)

• ATR-based stop loss calculation

• Risk-reward based take profit levels (1-5 targets)

• Visual lines and labels showing entry, SL, and TPs

• Automatically adapts to market volatility

• ⚠️ VISUAL REFERENCE ONLY - Does not execute trades

✅ SUPPORT & RESISTANCE DETECTION

• Automatic pivot-based level identification

• Red dashed lines for resistance zones

• Green dashed lines for support areas

• Helps identify key price levels

✅ VWMA TREND BANDS

• Volume-weighted moving average with standard deviation

• Color-changing bands (Green = Uptrend, Red = Downtrend)

• Filled band area for easy visualization

• Volume-confirmed trend strength

✅ TREND DETECTION SYSTEM

• Counting-based trend confirmation

• Three states: Up Trend, Down Trend, Ranging

• Requires threshold of consecutive bars

• Independent trend validation

✅ PRICE RANGE VISUALIZATION

• High/Low range lines showing market structure

• Filled area highlighting price volatility

• Helps identify breakout zones

✅ COMPREHENSIVE INFO TABLE

• Real-time trend status

• Last signal type (BUY/SELL)

• Entry price display

• Stop loss level

• All active take profit levels

• Clean, professional layout

✅ OPTIONAL FEATURES

• Bar coloring by trend direction

• Customizable alert notifications

• Toggle visibility for all components

• Fully configurable parameters

📊 HOW IT WORKS

═══════════════════════════════════════════════════════════════════

SIGNAL METHODOLOGY:

BUY SIGNAL generates when ALL conditions are met:

• Smoothed price > Moving Average (upward price trend)

• PVT > PVT Average (volume supporting uptrend)

• ROC > 0 (positive momentum)

• Close > VWMA (above volume-weighted average)

SELL SIGNAL generates when ALL conditions are met:

• Smoothed price < Moving Average (downward price trend)

• PVT < PVT Average (volume supporting downtrend)

• ROC < 0 (negative momentum)

• Close < VWMA (below volume-weighted average)

This multi-factor approach filters out weak signals and waits for

strong convergence before generating alerts.

RISK CALCULATION:

Stop Loss = Entry ± (ATR × SL Multiplier)

• Uses Average True Range for volatility measurement

• Automatically adjusts to market conditions

Take Profit Levels = Entry ± (Risk Distance × TP Multiplier × Level)

• Risk Distance = |Entry - Stop Loss|

• Creates risk-reward based targets

• Example: TP Multiplier 1.0 = 1:1, 2:2, 3:3 risk-reward

⚠️ NOTE: All risk levels are VISUAL REFERENCES for educational study.

They do not execute trades automatically.

⚙️ SETTINGS GUIDE

═══════════════════════════════════════════════════════════════════

SIGNAL SETTINGS:

• Signal Length (14): Main calculation period for averages

• Smooth Length (8): Price data smoothing period

• PVT Length (14): Price Volume Trend calculation period

• ROC Length (9): Rate of Change momentum period

RISK MANAGEMENT (Visual Only):

• ATR Length (14): Volatility measurement lookback

• SL Multiplier (2.2): Stop loss distance (× ATR)

• TP Multiplier (1.0): Risk-reward ratio per TP level

• TP Levels (1-5): Number of take profit targets to display

• Show TP/SL Lines: Toggle visual reference lines

SUPPORT & RESISTANCE:

• Pivot Lookback (10): Sensitivity for S/R detection

• Show SR: Toggle support/resistance lines

VWMA BANDS:

• VWMA Length (20): Volume-weighted average period

• Show Bands: Toggle band visibility

TREND DETECTION:

• Trend Threshold (5): Consecutive bars required for trend

PRICE LINES:

• Period (20): High/low calculation lookback

• Show: Toggle price range visualization

DISPLAY OPTIONS:

• Signals: Show/hide BUY/SELL labels

• Table: Show/hide information panel

• Color Bars: Enable trend-based bar coloring

ALERTS:

• Enable: Activate alert notifications for signals

💡 USAGE INSTRUCTIONS

═══════════════════════════════════════════════════════════════════

RECOMMENDED APPROACH:

• Works on all timeframes (1m to Monthly)

• Suitable for all markets (Stocks, Forex, Crypto, etc.)

• Best used with additional analysis and confirmation

• Always practice proper risk management

ENTRY STRATEGY:

1. Wait for BUY or SELL signal to appear

2. Check trend table for trend confirmation

3. Verify VWMA band color matches signal direction

4. Look for nearby support/resistance confluence

5. Consider entering on next candle open

6. Use visual SL level for risk management

EXIT STRATEGY:

1. Use TP levels as potential exit zones

2. Consider scaling out at multiple TP levels

3. Exit on opposite signal

4. Adjust stops as trade progresses

5. Account for spread and slippage

TREND TRADING:

• "Up Trend" → Focus on BUY signals

• "Down Trend" → Focus on SELL signals

• "Ranging" → Wait for clear trend or use range strategies

🎨 VISUAL ELEMENTS

═══════════════════════════════════════════════════════════════════

• GREEN VWMA BANDS → Bullish trend indication

• RED VWMA BANDS → Bearish trend indication

• ORANGE DASHED LINE → Entry price reference

• RED SOLID LINE → Stop loss level

• GREEN DOTTED LINES → Take profit targets

• RED DASHED LINES → Resistance levels

• GREEN DASHED LINES → Support levels

• GREY FILLED AREA → Price high/low range

• GREEN BUY LABEL → Long signal

• RED SELL LABEL → Short signal

• BLUE INFO TABLE → Current trade details

• GREEN/RED BARS → Trend direction (optional)

⚠️ IMPORTANT NOTES

═══════════════════════════════════════════════════════════════════

RISK WARNING:

• Trading involves substantial risk of loss

• You can lose more than your initial investment

• Past performance does not guarantee future results

• No indicator is 100% accurate

• Always use proper position sizing

• Never risk more than you can afford to lose

EDUCATIONAL PURPOSE:

• This tool is for learning and research

• Not a complete trading system

• Should be combined with other analysis

• Requires interpretation and context

• Test thoroughly before live use

• Consider consulting a financial advisor

TECHNICAL LIMITATIONS:

• Signals lag price action (all indicators lag)

• False signals occur in choppy markets

• Works better in trending conditions

• Support/resistance levels are approximate

• TP/SL levels are suggestions, not guarantees

📚 METHODOLOGY

═══════════════════════════════════════════════════════════════════

This indicator combines established technical analysis concepts:

• Price Volume Trend (PVT): Volume-weighted price momentum

• Rate of Change (ROC): Momentum measurement

• Volume-Weighted Moving Average (VWMA): Trend identification

• Average True Range (ATR): Volatility measurement (J. Welles Wilder)

• Pivot Points: Support/resistance detection

All methods are based on publicly available technical analysis

principles. No proprietary or "secret" algorithms are used.

⚖️ FULL DISCLAIMER

═══════════════════════════════════════════════════════════════════

LIABILITY:

The creator (Zakaria Safri) assumes NO liability for:

• Trading losses or damages of any kind

• Loss of capital or profits

• Incorrect signal interpretation

• Technical issues, bugs, or errors

• Any consequences of using this tool

USER RESPONSIBILITY:

By using this indicator, you acknowledge that:

• You are solely responsible for your trading decisions

• You understand the substantial risks involved

• You will not hold the creator liable for losses

• You will conduct your own research and analysis

• You may consult a licensed financial professional

• You are using this tool entirely at your own risk

AS-IS PROVISION:

This indicator is provided "AS IS" without warranty of any kind,

express or implied, including but not limited to warranties of

merchantability, fitness for a particular purpose, or non-infringement.

The creator is not a registered investment advisor, financial planner,

or broker-dealer. This tool is not approved or endorsed by any

financial authority.

📞 ABOUT THE CREATOR

═══════════════════════════════════════════════════════════════════

Created by: Zakaria Safri

Specialization: Technical analysis indicator development

Focus: Multi-factor analysis, risk visualization, trend detection

This is an educational tool designed to demonstrate technical

analysis concepts and multi-factor signal generation methods.

📋 VERSION INFO

═══════════════════════════════════════════════════════════════════

Version: 1.0

Platform: TradingView Pine Script v5

License: Mozilla Public License 2.0

Creator: Zakaria Safri

Year: 2024

═══════════════════════════════════════════════════════════════════

Study Carefully, Trade Wisely, Manage Risk Properly

TradeVision Pro - Educational Trading Tool

Created by Zakaria Safri

═══════════════════════════════════════════════════════════════════

Candle Body Break (M/W/D/4H/1H)v5# Candle Body Break (M/W/D/4H/1H) Multi-Timeframe Indicator

This indicator identifies and plots **Candle Body Breaks** across five key timeframes: Monthly (M), Weekly (W), Daily (D), 4-Hour (4H), and 1-Hour (1H).

## Core Logic: Candle Body Break

The core concept is a break in the swing high/low defined by the body of the previous counter-trend candle(s). It focuses purely on **closing price breaks** of remembered highs/lows established by full candle bodies (close > open or close < open).

1. **Remembering the Swing:**

* After a bullish break (upward trend), the indicator waits for the first **bearish (close < open) candle** to appear. This bearish candle's high (`rememberedHigh`) and low (`rememberedLow`) are saved as the **breakout level**.

* Subsequent bearish candles that make a new low update this saved level, continuously adjusting the level to the most significant recent resistance/support established by the body's range.

2. **Executing the Break:**

* **Bull Break (Long signal):** Occurs when a **bullish candle's closing price** exceeds the last remembered bearish high (`rememberedHigh`).

* **Bear Break (Short signal):** Occurs when a **bearish candle's closing price** falls below the last remembered bullish low (`rememberedLow_Bull`).

Once a break occurs, the memory is cleared, and the indicator waits for the next counter-trend candle to establish a new level.

## Features

* **Multi-Timeframe Analysis:** Displays break lines and labels for M, W, D, 4H, and 1H timeframes on any chart.

* **Timeframe Filtering:** Break lines are only shown for timeframes **equal to or higher** than the current chart timeframe (e.g., on a 4H chart, only 4H, D, W, and M breaks are displayed).

* **Candidate Lines (Dotted Green):** Plots the current potential breakout level (the remembered high/low) that must be broken to trigger the next signal.

* **Direction Table:** A table in the top right corner summarizes the latest break direction (⇧ Up / ⇩ Down) for all five timeframes. This can be optionally limited to the 4H chart only.

* **1H Alert:** Triggers an alert when a 1-Hour break is detected.

## Input Settings Translation (for Mod Compliance)

| English Input Text | Original Japanese Text |

| :--- | :--- |

| **Show Monthly Break Lines** | 月足ブレイクを描画する |

| **Show Weekly Break Lines** | 週足ブレイクを描画する |

| **Show Daily Break Lines** | 日足ブレイクを描画する |

| **Show 4-Hour Break Lines** | 4時間足ブレイクを描画する |